But before transactions are posted to the T-accounts, they are first recorded using special forms known as journals. For example, ABC International issues 20 invoices to its customers over a one-week period, for which the totals in the sales subledger are for sales of $300,000. ABC’s controller creates a posting entry to move the total of these sales into the general ledger with a $300,000 debit to the accounts receivable account and a $300,000 credit to the revenue account. Also, Ledger posting segregates the nature of accounts and their balances which helps in making the financial statements i.e trial balance, profit and loss account and balance sheet.

Once the accounting period has ended and all transactions have been recognized, documented, and posted to the ledger, this is the initial action that is taken.

The video provides a clear description of where in the accounting cycle posting occurs.

When each entry is posted its ledger account the journal entry number is usually placed next to the entry in the T-account.

Trump has regularly railed about the case on his Truth Social platform.

The business can learn the unadjusted balances in each account from a trial balance.

When calculating balances in ledger accounts, one must take into consideration which side of the account increases and which side decreases.

The Post accounting process refers to the process of transferring all transactions from all Journals (transaction records) to the Chart of Accounts. Post-accounting can also apply to moving one or more transactions from a module into a Journal. Since posting to the ledger is a manual procedure, labour is required. It guarantees that all assets and liabilities will be accurately documented. Nominal account amounts are immediately moved from the nominal account to the profit and loss account.

Company

These reports have much more information than the financial statements we have shown you; however, if you read through them you may notice some familiar items. Another key element to understanding the general ledger, and the third step in the accounting cycle, is how to calculate balances in ledger accounts. Recall that the general ledger is a record of each account and its balance. Reviewing journal entries individually can be tedious and time consuming. The general ledger is helpful in that a company can easily extract account and balance information.

There can be two accounts in the debit and one in the credit or one in the debit and two in credit part. However, the rule of posting is the same in this case too, but care should be taken while posting the amounts. An accounting ledger refers to a book that consists of all accounts used by the company, the debits and credits under each account, and the resulting balances. Let us illustrate how accounting ledgers and the posting process work using the transactions we had in the previous lesson. After journal entries are made, the next step in the accounting cycle is to post the journal entries into the ledger. Posting refers to the process of transferring entries in the journal into the accounts in the ledger.

Position Details

As a result, the final balance will be debit minus credit on the last date i.e $15000. The real estate tycoon listened intently to testimony from Bartov, who opined that the AG’s case has “no merit,” dismissing any what is posting in accounting errors in Trump’s annual financial statements as par for the course. Deutsche Bank executives have testified that, while expecting clients to provide broadly accurate information, they often adjust the numbers.

You can use Synder’s ecommerce analytics and reporting option to have a deeper and broader look at your business’s performance, including sales, customers, and products. You can assess your overall performance or break it down by channels. You can track critical ecommerce KPIs, customer behavior patterns, and product performance to understand your business’s dynamics and elaborate actionable strategies for profitability and growth. QuickBooks is one of the most widely used accounting software in the US and worldwide. Created by Intuit, it aims to help businesses manage their financial tasks efficiently, including bookkeeping, invoicing, payroll, and tax preparation.

The two main options you have are cash accounting and accrual accounting. Although e-commerce accounting software will typically let you choose either method, many default to accrual accounting. Magento’s benefit, as mentioned, is its extensive customization options. This platform is the king of plugins – you can find a plugin for whatever you want to improve or introduce in your store.

Using online marketplaces

Besides, here, you might want to add all the payment processors you use to receive payments. For example, you can set up Smart Rules to automatically categorize transactions based on certain criteria, such as transaction amount, description, or payment method. Ecommerce integrations listed below can connect to QuickBooks Online either through built-in or third-party solutions. It can pose several challenges (I’ll talk about those a bit further on), but we’ll get to how you can address them.

PayPal, Square, Stripe, and others can be connected directly to your QuickBooks account.

It automatically converts transactions made in different currencies into the business’s base currency, simplifying accounting for international sales.

Additionally, Ecwid offers integrations with various online platforms and marketplaces, allowing users to reach customers wherever they are.

It saves the day, as you don’t have to search for third-party solutions, helping you introduce ecommerce functionality to your website and add another app to your business toolset to learn and manage.

A sales funnel is simply a visual representation of the sales process.

For more information about Expert Assisted, refer to the QuickBooks Terms of Service.

Connect all the dots

Ultimately, you may want to speak to an accountant before deciding. E-commerce accounting is the process of recording, tracking, and analyzing financial transactions that occur within an online business. The process might slightly change from software to software, but, as I mentioned, the basics are pretty much similar. You sign up, add your ecommerce platform and QuickBooks account, and go through the settings to finalize the integration. Backup is important, so never skip it, as well as testing the integration on a small bit of data before a full-blown sync. It’s ridiculously simple – using a single solution to integrate whichever ecommerce platforms and payment processors you might be using with QuickBooks.

BigCommers offers plenty of templates you can choose from to design your store. It allows for adding products, configuring payment gateways, and setting up pricing and shipping options. The admin dashboard within BigCommerce is where you manage orders, track inventory levels, and monitor sales performance. Shopify is a popular ecommerce platform that enables businesses to create and customize online stores to sell products.

E-commerce accounting basics

BigCommerce offers native integration options that allow users to sync orders, customers, and inventory data directly with QuickBooks Online. Sellers can configure the integration settings within the BigCommerce dashboard to ensure seamless synchronization between the two platforms. It eliminates the need for third-party plugins and simplifies managing financial data. BigCommerce’s robust built-in feature set is its outstanding advantage. Unlike other platforms that rely heavily on third-party apps, BigCommerce offers a wide range of built-in functionalities that cater to various ecommerce needs. From multi-channel selling and inventory management to advanced SEO tools and marketing automation – BigCommerce provides everything businesses might need to succeed online.

To attract potential customers, you’ll need a solid understanding of your target market.Researching your audience and their buying habits allows you to determine how best to reach this group. Pick a platform and launch your custom store through the vendor’s site. Whether you’re a new entrepreneur or you’re looking for ways to expand your business, check out these e-commerce trends to know.

If you run an online store, you know how important it is to keep track of your the origins of lehman’s ‘repo 105’ finances. But e-commerce accounting is more than just tracking accounts payable and recording sales and expenses. It’s also understanding how your business operates, what drives your profitability, and how to plan for the future. Starting with Etsy is pretty straightforward – you sign up for an Etsy seller account and create product listings.

The acid-test ratio is a financial metric that evaluates a company’s short-term liquidity position. By focusing on assets that can be quickly converted to cash, it determines whether a company can meet immediate liabilities without relying on inventory sales. This measure is crucial for investors and creditors assessing a business’s financial health. The acid test ratio measures the liquidity of a company by showing its ability to pay off its current liabilities with quick assets. If a firm has enough quick assets to cover its total current liabilities, the firm will be able to pay off its obligations without having to sell off any long-term or capital assets. The acid-test, or quick ratio, shows if a company has, or can get, enough cash to pay its immediate liabilities, such as short-term debt.

The acid test ratio, or quick ratio, evaluates a company’s ability to meet short-term obligations without relying on inventory sales. Cash processing non-po vouchers and cash equivalents are the most direct components, representing funds accessible immediately. Marketable securities, such as government bonds or stocks, are included due to their quick saleability in financial markets. Accounts receivable, while not as liquid as cash, are considered quick assets because they represent money expected to be collected soon. This approach offers a conservative view of a company’s liquidity, providing a realistic picture of its ability to cover short-term liabilities. Higher quick ratios are more favorable for companies because it shows there are more quick assets than current liabilities.

These benchmarks can be sourced from financial databases like Bloomberg or industry reports from organizations such as Deloitte. A declining acid test ratio could point to emerging liquidity issues, while an improving ratio might indicate successful financial management strategies. Stakeholders should also consider external factors, such as economic conditions, that can influence a company’s liquidity position. Conversely, a ratio below 1 may signal potential liquidity concerns, indicating the company might struggle to meet short-term obligations.

What Is the Difference Between Liquidity and Solvency?

The acid-test ratio is used to indicate a company’s ability to pay off its current liabilities without relying on the sale of inventory or on obtaining additional financing. Inventory is not included in calculating the ratio, as it is not ordinarily an asset that can be easily and quickly converted into cash. Compared to the current ratio – a liquidity or debt ratio which does include inventory value in the calculation – the acid-test ratio is considered a more conservative estimation of a company’s financial health.

Acid Test Ratio

Other elements that appear as assets on a balance sheet should be subtracted if they cannot be used to cover liabilities in the short term, such as advances to suppliers, prepayments, and deferred tax assets. Comparing it against industry benchmarks is essential to truly understand a company’s liquidity position. Each industry has unique characteristics, and liquidity norms can vary significantly. For example, industries with rapid cash flow cycles, such as technology, often function well with lower ratios compared to capital-intensive sectors like manufacturing, where higher liquidity is generally expected. To calculate the acid-test ratio of a company, divide a company’s current cash, marketable securities, and total accounts receivable by its current liabilities.

Cash, cash equivalents, short-term investments or marketable securities, and current accounts receivable are considered quick assets.

Service-oriented businesses, such as consulting firms, usually maintain ratios above 1.2 due to limited inventory and tangible assets.

The acid-test ratio is more conservative than the current ratio because it doesn’t include inventory, which may take longer to liquidate.

Most importantly, inventory should be subtracted, keeping in mind that this will negatively skew the picture for retail businesses because of the amount of inventory they carry.

Calculating quick assets involves identifying and summing up components readily convertible into cash.

Useful tips for Using the Acid Test Ratio

Upgrading to a paid membership gives you access to our extensive collection of plug-and-play Templates designed to power your performance—as well as CFI’s full course catalog and accredited Certification Programs. Double Entry Bookkeeping is here to provide you with free online information to help you learn and understand bookkeeping and introductory accounting. Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses!

What are the limitations of the acid test ratio?

My Accounting Course is a world-class educational resource developed by experts to simplify accounting, finance, & investment analysis topics, so students and professionals can learn and propel their careers. Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching. After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career.

Businesses often balance risk and return by investing in a diversified portfolio of securities to strengthen their liquidity position. Accounts receivable represent payments owed by customers for goods or services rendered. Strategies like offering early payment discounts or conducting credit checks can improve collection efficiency.

To begin, gather the company’s financial statements, typically the balance sheet, to locate relevant figures.

Conversely, a ratio below 1 may signal potential liquidity concerns, indicating the company might struggle to meet short-term obligations.

Upgrading to a paid membership gives you access to our extensive collection of plug-and-play Templates designed to power your performance—as well as CFI’s full course catalog and accredited Certification Programs.

The acid test provides a back-of-the-envelope calculation to see if a company is liquid enough to meet its short-term obligations.

Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching.

No single ratio will suffice in every circumstance when analyzing a company’s financial statements.

What Is the Difference Between the Current Ratio and the Acid-Test Ratio?

If it’s less than 1.0, then companies do not have enough liquid assets to pay their current liabilities and should be treated with caution. If the acid-test ratio is much lower than the current ratio, it means that a company’s current assets are highly dependent on inventory. On the other hand, a very high ratio could indicate that accumulated cash is sitting idle rather than being reinvested, returned to shareholders, or otherwise put to productive use. The Acid-Test Ratio, also known as the quick ratio, is a liquidity ratio that measures how sufficient a company’s short-term assets are to cover its current liabilities.

Gain insights into the acid test ratio, its calculation, and interpretation to assess a company’s short-term financial health effectively. Secondly in example 2 above the ratio is 0.69 and the business is only able to generate cash of 0.69 for every 1 it owes. Clearly in the unlikely event of all current liabilities being demanded at the same time the business would be unable to make payment. Understand the acid-test ratio, its calculation, and its significance in assessing a company’s short-term financial health.

Understanding the Acid-Test Ratio

No single ratio will suffice in every circumstance when analyzing a company’s financial what does janitorial expense means statements. It’s important to include multiple ratios in your analysis and compare each ratio with companies in the same industry. The acid-test ratio can be impacted by other factors such as how long it takes a company to collect its accounts receivables, the timing of asset purchases, and how bad-debt allowances are managed. The logic here is that inventory can often be slow moving and thus cannot readily be converted into cash. Additionally, if it were required to be converted quickly into cash, it would most likely be sold at a steep discount to the carrying cost on the balance sheet.

Quick Ratio

Liquidity is among one of the most important aspects of a company and its long-term viability.

Compared to the current ratio, the acid test ratio is a stricter liquidity measure due to excluding inventory from the calculation of current assets. The information we need includes Tesla’s Q cash & cash equivalents, receivables, and short-term investments how to report and pay taxes on 1099 in the numerator; and total current liabilities in the denominator. The ratio’s denominator should include all current liabilities, debts, and obligations due within one year. If a company’s accounts payable are nearly due but its receivables won’t come in for months, it could be on much shakier ground than its ratio would indicate. Cash and cash equivalents form the foundation of quick assets, including currency on hand, demand deposits, and short-term investments easily liquidated without significant loss.

The average book value refers to the average between the beginning and ending book value of the investment, such as the acquired fixed asset. Return on sales (ROS) is the metric that answers, « How much do we keep of every dollar we make in sales? » Let’s discuss why that’s important, how it’s calculated, and how you can maximize this ROS to give your business a boost. For tax purposes, interest is commonly defined as “compensation for the use or forbearance of money,” based on the Supreme Court’s decision in Deputy v. du Pont, 308 U.S. 488 (1940). The Supreme Court further held in Midland–Ross Corp., 381 U.S. 54 (1965), that “earned OID serves the same function as stated interest” and thus should be treated akin to interest. Chartered accountant Michael Brown is the founder and CEO of Double Entry Bookkeeping.

Differences Between Events and Transactions

The Accounting Rate of Return (ARR) provides firms with a straight-forward way to evaluate an investment’s profitability over time. A firm understanding of ARR is critical for financial decision-makers as it demonstrates the potential return on investment and is instrumental in strategic planning. Investment evaluation, capital budgeting, and financial analysis are all areas where ARR has a strong foundation. Its adaptability makes it useful for a wide range of applications, including assessing the economic profitability of projects, benchmarking performance, and improving resource allocation.

Determine the initial investment cost

The Accounting Rate of Return is a simple yet powerful metric for evaluating investment profitability. Its ease of use and alignment with accounting figures make it a popular choice for businesses and investors alike. Based on the below information, you are required to calculate the accounting rate of return, assuming a 20% tax rate. Below is the estimated cost of the project, along with revenue and annual expenses. However, the formula doesn’t take the cash flow of a project or investment into account. It should therefore always be used alongside other metrics to get a more rounded and accurate picture.

Company Overview

He has worked as an accountant and consultant for more than 25 years and has built financial models for all types of industries. He has been the CFO or controller of both small and medium sized companies and has run small businesses of his own. He has been a manager and an auditor with Deloitte, a big 4 accountancy firm, and holds a degree from Loughborough University. The average investment in the project over the three years is therefore 87,000.

For example, a small business evaluating equipment purchases may find ARR sufficient for preliminary comparisons, reserving more complex metrics for high-stakes decisions. Understanding the Accounting Rate of Return (ARR) is essential for businesses evaluating potential investments. As a straightforward metric, ARR provides insight into the profitability of an investment relative to its cost, making it a valuable tool for decision-makers seeking to allocate resources efficiently. Return on sales is the ratio of operating profit to net sales, demonstrating how much of your revenue translates to profit. If properly identified, a hedging transaction under Sec. 1221 results in ordinary income, deduction, gain, or loss to a taxpayer because it would not constitute a capital asset. For tax purposes, the term “debt issuance costs” means transaction costs incurred by an issuer of debt that are required to be capitalized under Regs.

The answer to this question is « It depends. » It’s relative to the company’s size and its industry, as these can vary wildly across sectors.

The denominator in the formula is the amount of investment initially required to purchase the asset.

In practice, other methods are used if their results do not differ materially from the interest method, such as a straight–line amortization method.

This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business.

This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services.

Each of these approaches has distinct advantages and disadvantages, but they are all used to determine the property’s fair market value.

Accounting rate of return

If you can match or undercut that perceived value, you can compete on these prices. It requires clear communication of your product benefits and strong customer relationships. You could also use channel sales through partnerships to increase value for all parties. Hotels’ ROS is affected by location, brand, and operational costs, such as staffing, utilities, and maintenance. Luxury hotels and resorts tend to have higher ROS because their fees rise disproportionately to increased operational costs, while budget or economy hotels might see lower ROS.

One such tool is the Accounting Rate of Return (ARR) method, which offers a straightforward approach to assessing the profitability of an investment. So, what exactly is the ARR method, and how can it help in making informed investment decisions? The accounting rate of return, or ARR, is another method of investment appraisal. The accounting rate of return measures the profit generated compared to the initial investment. ARR does not account for the time value of money or focus on cash flows, which can lead to incomplete evaluations for long-term investments. It also relies on averages, potentially oversimplifying projects with fluctuating returns.

Most notably, debt issuance costs and hedging gain or loss may be included as interest expense for accounting purposes but may not constitute interest expense for tax purposes. On the other hand, some fees paid to lenders may constitute OID for tax purposes and not debt issuance costs, despite being labeled as a fee. The accounting rate of return can be calculated by dividing the earnings generated on an investment by the amount of money invested. The accounting rate of return is a method of calculating a projects return as a percentage of the investment in the project. It measures the accounting profitability and takes no account of the time value of money. The Accounting Rate of Return (ARR) is a straightforward yet valuable metric for assessing the profitability of an investment.

Similarly, the straight–line method or other methods may be permissible general sales taxes and gross receipts taxes for tax purposes under certain circumstances. Small businesses often have limited resources and need quick, easy-to-understand methods for evaluating investments. ARR can help them make initial decisions on projects like purchasing new equipment, expanding operations, or launching new products.

( : Computation of accounting rate of return:

The choice of depreciation method, such as straight-line or an accelerated approach like double-declining balance, can alter annual profit figures. For example, accelerated depreciation under MACRS may reduce net income in the early years of an investment, affecting ARR. The depreciation method applied to the investment will influence net income and, therefore, the ARR.

When projects vary significantly in these aspects, ARR operating cash flow calculation may not provide an accurate comparison, leading to suboptimal investment decisions. This means the project is expected to generate a 20% return on investment each year. The three kinds of investment evaluation methodologies are discounted cash flow (DCF), comparative sales analysis (CSA), and market approach. Each of these approaches has distinct advantages and disadvantages, but they are all used to determine the property’s fair market value.

By comparing the expected profitability of different projects, they can allocate resources more effectively to enhance their offerings.

This strategy is advantageous because it examines revenues, cost savings, and costs related to the investment.

The Accounting Rate of Return (ARR) is the average net income earned on an investment (e.g. a fixed asset purchase), expressed as a percentage of its average book value.

The Accounting Rate of Return (ARR) method is a simple yet effective tool for evaluating the profitability of investments.

This makes NPV particularly useful for long-term projects with varying cash flows.

First, taxpayers should comprehensively analyze the composition of interest expense for accounting purposes to determine whether it is interest for tax purposes.

A closer look at the costs of borrowing

Furthermore, the accounting rate of return does not account for changes in market conditions or inflation. Therefore, it is important to use this metric in conjunction with other financial analysis tools to make sound investment decisions. Accounting rate of return is the estimated accounting profit that the company makes from investment or the assets. It is the percentage of average annual profit over the initial investment cost.

The average net income used in the formula is calculated by taking the total net income for the project (which allows for the depreciation expense on the investment) and dividing this by the term in years of the project. Whether the investments are short-term CDs or long-term retirement plans, investments play a big role in Americans’ lives. The only way to tell whether an investment is worthwhile or not is to measure the return or amount of money the investment has made and is expected to make in the future. An ARR of 10% for example means that the investment would generate an average of 10% annual accounting profit over the investment period based on the average investment. Despite these limitations, ARR’s simplicity and reliance on readily available accounting data make it easier to calculate and interpret, especially for smaller businesses or initial analyses.

Discount or premium is reported on the balance sheet as a direct deduction or addition, respectively, to the face amount of a debt. Similarly, debt issuance costs related to a debt are reported on the balance sheet as a direct deduction from the face amount. However, interest may include imputed interest under the accounting rules, despite the actual terms, when the transaction is viewed as not at arm’s length or the market rate materially differs from the stated interest rate. If they differ significantly, use other methods that can better account for these variations.

The disadvantage of the ARR technique is that it takes no account of the time value of money, the net income over the period of the project is simply averaged. There are two main rules to be used for making decisions when using the ARR method to calculate project returns. The accounting rate of return method shows that the return on this project is 20% a year for 3 years.

This strategy is advantageous because it examines revenues, cost savings, and costs related to the investment. In certain situations, it can offer a full picture of the impact instead of relying just on cash flows generated. The accounting rate of return is a capital budgeting indicator that may be used to swiftly and easily determine the profitability of a project. Businesses generally utilize ARR to compare several projects and ascertain the expected rate of return for each one. If you have already studied other capital budgeting methods (net present value method, internal rate of return method and payback method), you may have noticed that all these methods focus on cash flows. But accounting rate of return (ARR) method uses expected net operating income to be generated by the investment proposal rather than focusing on cash flows to evaluate an investment proposal.

CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path. Return on sales is made up of many parts (which also need to be calculated before getting to your ROS). By granting them a profits interest, entities taxed as partnerships can reward employees with equity. For items listed in the general category, the regulations provide a nonexclusive list of items including QSI, OID, de minimis OID, and repurchase premium. sample chart of accounts for a small company Notwithstanding that a hedging transaction will be linked to the hedged item by Sec. 1221 and Regs.

The numbering system is like a code that is given to every account type. This code then hierarchically flows to its sub-accounts to categorize transactions that can be easily referenced. The income statement contains operating revenues, https://quick-bookkeeping.net/ operating expenses, non-operating revenues and gains, and non-operating expenses and losses. The income statement accounts are used to generate the other major kind of financial statement which is known as the income statement.

A chart of accounts showcases all accounts according to the order they follow in the financial statements.

Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others.

Ideally, account descriptions should be concise but allow for the inclusion of several relevant accounts.

With NetSuite, you go live in a predictable timeframe — smart, stepped implementations begin with sales and span the entire customer lifecycle, so there’s continuity from sales to services to support.

Liability accounts also follow the traditional balance sheet format by starting with the current liabilities, followed by long-term liabilities.

The complete Swedish BAS standard chart of about 1250 accounts is also available in English and German texts in a printed publication from the non-profit branch BAS organisation. The Spanish generally accepted accounting principles chart of accounts layout is used in Spain. The French generally accepted accounting principles chart of accounts layout is used in France, Belgium, Spain and many francophone countries. The use of the French GAAP chart of accounts layout (but not the detailed accounts) is stated in French law. Accounts may be added to the chart of accounts as needed; they would not generally be removed, especially if any transaction had been posted to the account or if there is a non-zero balance. The charts of accounts can be picked from a standard chart of accounts, like the BAS in Sweden.

Why is the chart of accounts important?

And to find the exact number, you might have to sift through months’ worth of invoices. In the worst-case scenario, discovering that your file system was disorganized will set you up for failure. You may also find contingent liabilities or those whose occurrence depends on a certain event. Contingent liabilities are basically potential liabilities in that they may or may not happen. For example, if a company faces a lawsuit, it may or may not be a liability depending on the outcome of the lawsuit.

It also makes it easier to check specific accounts quickly, as accounts are separated into assets, liabilities, equity, revenue, costs of goods and expenses.

For example, if ABC Company sells merchandise to a customer, it would record the transaction in the sales revenue account under the revenue category.

Of crucial importance is that COAs are kept the same from year to year.

Our partners cannot pay us to guarantee favorable reviews of their products or services.

A chart of accounts, or COA, is a complete list of all the accounts involved in your business’s day-to-day operations.

You use a COA to organize transactions into groups, which in turn helps you track money coming in and out of the company. It is a very important financial tool that organizes a lot of financial transactions in a way that is easy to access. Because transactions are displayed as line items, they can quickly be found and assessed. This is crucial for providing investors and other stakeholders a bird’s-eye view of a company’s financial data. If you need help with your company’s chart of accounts, EcomBalance can help. At EcomBalance, we provide accounting and bookkeeping services and help your team chase invoice payments automatically, reducing the amount of paperwork they need to do.

Which of these is most important for your financial advisor to have?

It may make sense to create separate line items in your chart of accounts for different types of income. A chart of accounts is a catalog of account names used to categorize transactions and keep your business’s financial history organized. The list typically displays account names, details, codes and balances. There’s often an option to view all the transactions within a particular account, too.

Chart of accounts best practices

The first digit might, for example, signify the type of account (asset, liability, etc.). In accounting software, using the account number may be a more rapid way to post to an account, and allows accounts to be presented in numeric order rather than alphabetic order. It helps to categorize all transactions, working as a simple, at-a-glance reference point. Similar to a chart of accounts, an accounting template can give you a clear picture of your business’s financial information at a glance.

( Make Your Reports Better

A chart of accounts is a comprehensive and structured list of all the accounts used in a business’s ledger. Large businesses also use account numbers or codes that contain vital information. For example, 501S may be assigned for salary expenses incurred by the selling department, and 501A for salary expenses of the administrative office. The account code is typically a three-digit https://business-accounting.net/ code to describe the account itself. Each major category starts with a particular number and all of the subcategories of fall under a certain category start with the number of the major category. Accounting standards say that a company needs to only record contingent liabilities if the liability is probable and if it’s possible to reasonably estimate the amount.

Business is Our Business

Here are tips for how to do this, plus details about what a COA is, examples of a COA and more. To make it easy for readers to locate specific accounts or to know what they’re looking at instantly, each COA typically contains identification codes, names, and brief descriptions https://kelleysbookkeeping.com/ for accounts. But the final structure and look will depend on the type of business and its size. An organized, descriptive COA can help bookkeepers, accountants, and financial managers make informed business decisions based on relevant, accurate, and timely data.

A well-designed chart of accounts should separate out all the company’s most important accounts, and make it easy to figure out which transactions get recorded in which account. Different industries have unique financial reporting requirements, and businesses must ensure that their COA reflects those requirements. For example, in contrast to service-based businesses, manufacturers may need to monitor inventory levels and the cost of goods sold. It offers a methodical technique to classify and arrange financial data, making it simpler for businesses to produce financial reports and evaluate their financial performance.

This means you may need to take additional actions, such as accounting for earnings before taxes and interest, and making adjustments for non-operating expenses such as accounts payable and depreciation. Unlike the direct method, the indirect method provides less detailed information about specific cash flow activities. It doesn’t offer a deep understanding of what contributes to the company’s net cash flows. This method is useful because it shows why your profit differs from your closing bank balance. However, it lacks detailed insights into specific cash transactions and their sources, which means you might miss important information about your finances.

If you’re reporting month-on-month, a $30,000 sale closing at the end of the month but not getting paid out until the following month can complicate your reporting.

However, there will be scenarios where it will be advantageous to choose one over the other.

So make sure you choose the method that puts you in the best place to help your business succeed.

If you want to use this method, you need to keep separate records for your cash transactions and for your credit or value transactions.

In general, the two sets of standards are consistent between the statement of cash flows.

There are many advantages to preparing a cash flow statement using the indirect method.

Thus, prioritizing the importance of understanding the cash flow information as it provides meaningful insights for financial planning, management, and decision-making processes. Accounting standards allow users to present the cash flows from operating activities using either the direct method or the indirect method. Direct method is the preferred approach, but most companies use the indirect method for preparing cash flow statement because it is easier to implement.

Free Accounting Courses

If you’re reporting to internal stakeholders, you should use whichever method is easier to produce and for your audience to read. You should use the direct method if you’re reporting to investors, banks, or prospective buyers. Accrual method accounting recognizes revenue when earned, not when cash is received. If you’re reporting month-on-month, a $30,000 sale closing at the end of the month but not getting paid out until the following month can complicate your reporting.

This method also requires less preparation time, but the accuracy of the calculation is significantly lower.

The offset was sitting in the accounts receivable line item on the balance sheet.

The main difference between these 2 statements is how they calculate operating cash flow.

Accrual accounting states that revenue and expenses should be recognized when earned or incurred.

You also need to list any investments, such as new purchases and the sale of certain assets.

Examples of indirect costs include fixed costs that are relatively stable over time. The indirect method is relatively complex method as compared to the direct method as it utilizes net income as the base and performs necessary cashflow adjustments. One of the adjustments can be regarded as the treatment of non-cash https://quick-bookkeeping.net/ expenses. In indirect method, depreciation which is a non-cash expense is generally added back to the net income followed by additions and deductions arising from the changes in liabilities and assets. The direct method also enables businesses to compare their cash flow to competitors’ within the same industry.

High cash outflow for activities like repayment of loans could be indicative of decreasing liabilities. This could potentially lower the risk for the creditor, leading to improved credit terms for the business. The direct method of presenting the Cash Flow statement is often lauded for its transparency. By presenting cash inflows and outflows from unique operational activities individually, this method gives stakeholders a more detailed view of how a company’s operations are generating cash.

Head to Head Comparison between Direct vs Indirect Cash Flow Methods (Infographics)

Larger, more complex firms, on the other hand, may find it too inefficient to devote the necessary resources to the direct method, so the indirect alternative becomes faster and simpler. This option may also be more beneficial for long-term planning, as it gives a wider overview of the firm’s overall cash flow. The indirect method, by contrast, means reports are often easier to prepare as businesses typically already keep records on an accrual basis, which provides a better overview of the ebb and flow of activity. If you’re preparing a statement for shareholders and stakeholders who want to know where the company currently stands in terms of its cash flow, the direct method is the easiest one to understand.

What are the advantages and disadvantages of indirect cash flow?

It may not always get the most love, but your cash flow statement is a vital part of your reporting story. That’s why, in this post, we’re going to talk all about choosing the best cash flow method for your business. A direct cash flow statement is a simple representation of cash movement. The layout of the direct cash flow method makes it easy for the reader to understand how cash comes into and out of the business.

Advantages and disadvantages of each method

There would need to be a reduction from net income on the cash flow statement in the amount of the $500 increase to accounts receivable due to this sale. The cash flow statement is an important financial tool for any business. With this, the direct and indirect methods respectively offer different perspectives on cash flow calculation. https://kelleysbookkeeping.com/ From a creditor’s perspective, a detailed breakdown of cash flows via the direct method can assist in assessing a company’s ability to meet its obligations. Creditors, specifically, would focus on cash inflows from operations as a measure of the company’s ability to generate enough cash to pay off its current obligations.

However, the direct approach can still be viable if the company has lots of transactions that affect cash. Accounting software can easily categorize cash transactions so that they are quickly accessible when it comes time to prepare the cash flow statement using the direct method. Like the direct method, there are both advantages and disadvantages to this method.

The following steps listed below show you how to prepare a cash flow statement using the indirect method. If you are preparing a cash flow statement using the indirect method, you can follow these steps. A cash flow statement using the indirect method differs from the direct method of preparing a cash flow statement. There are many advantages to preparing a cash flow statement using the indirect method. Listing out information this way provides the financial statement user with a more detailed view of where a company’s cash came from and how it was disbursed. For this reason, the Financial Accounting Standards Board (FASB) recommends companies use the direct method.

You do not need to include other information from the company’s income statement. The direct method is perhaps the simplest to understand, though it’s often more complex to calculate in practice. However, the Financial Accounting Standards Board (FASB) prefers companies use the direct method as it https://bookkeeping-reviews.com/ offers a clearer picture of cash flows in and out of a business. However, if the direct method is used, it is still recommended to do a reconciliation of the cash flow statement to the balance sheet. The indirect method is one of two accounting treatments used to generate a cash flow statement.

We also read through tons of Oracle NetSuite reviews from actual users to see what customers like and dislike about it. Finally, we used our standardized rubric to grade NetSuite against the competition. While Acumatica has similar features to other ERPs, like various financial modules, it uses a different pricing model. But Acumatica has you pay for the data you consume rather than charging an annual (or monthly) license. That can make Acumatica a better value than NetSuite for some businesses. As an additional bonus, Acumatica offers pre-configured versions for specific industries.

That can be crucial for larger businesses expanding across borders.

Manufacturing and production entities will find extensive Bill of Materials (BoM) capabilities including kitting, which extends the BoM granularity to sub-assemblies (or « kits ») employed as a line item in a BoM.

NetSuite developers have managed to accomplish this without making you feel claustrophobic, like you do in some screens in Microsoft Dynamics GP.

Labeled Verified, they’re about genuine experiences.Learn more about other kinds of reviews.

Its comprehensive technology collection, built-in integrations, accounting features, integrations and e-commerce functions eliminate the need for multiple platforms.

The system can also cope with different pricing strategies, including volume discounts, promotional discounts and regional pricing differences. For example, you don’t get the built-in email marketing and phone functionality we evaluated in our review of Zoho CRM. Implementing anything new is very difficult; in house implementation teams are poor; feel nickeled and dimed every time we need something (quarterly check ins are really disguised sales opportunities). The system is customizable, yet the majority of the NFP products meets our needs without further customization. On many screens, there’s a row of additional links below the toolbar in a horizontal bar.

Oracle NetSuite Setup

We chose Oracle NetSuite as our top accounting software for advanced features because it’s a full-scale ERP platform. This means that accounting is only one area the software covers; you can also use it to manage all of your business’s other resources. Unlike QuickBooks Online Advanced, a top contender in the space, Oracle NetSuite doesn’t limit the number of users, and its reports are more advanced than QuickBooks’.

By compiling data, CRM enables you to know each customer’s preferences before you add the personal touch. NetSuite even lets you use AI to automate processes, saving you even more time. A handful of ERP vendors, like Oracle Fusion Cloud ERP and SAP S/4HANA, have a similar feature ― but it still sets NetSuite apart from your run-of-the-mill ERP system.

NetSuite

Ted Needleman has been covering the world of technology for almost 40 years. He writes frequently on software, hardware, and technology-related subjects. He has been a programmer, accountant, Editor-in-Chief of Accounting Technology magazine, and the director of an imaging and printing test lab. Even smaller SMEs may need these capabilities if they are operating or producing in other countries, and it’s nice that Oracle NetSuite OneWorld gives them that option. Inventory records can contain an image of the item, which is handy when you have items that are similar but not identical. NetSuite includes bin tracking for pick lists and, for those who need bar coding, that’s also supported.

That’s not unusual for software in this space, but it is something you need to budget for when choosing ERP software. This description might make Oracle NetSuite OneWorld sound more complex than it really is once you stop reading and actually put cursor to screen. There’s a logical and orderly progression netsuite reviews of mouse clicks that quickly brings you to the transaction or report you need. It’s not quite as visually intuitive as Intacct, but go through it a few times and you should be quite comfortable. And if you’re working for a company that uses Netsuite, I highly recommend re-evaluating your life choices.

Outside of these items, it is better to develop a detailed, line-by-line forecast that incorporates other factors than just the sales level. This more selective approach tends to yield budgets that more closely predict actual results. With the percentage of sales method, you can quickly forecast financial changes to your business percentage of sales method example — including both assets and expenses — based on previous sales history. This allows you to adjust budgets, strategies, and resourcing to ensure you hit desired targets. Multiply the total accounts receivable by the historical uncollected accounts percentage to predict how much these bad debts might cost for the time period.

Example of the Percent of Sales Method

When questioned on the topic, entrepreneur and angel investor Tim Berry, recommended that start-ups try to discover the percentage used by similar businesses. He suggests calling colleagues at a few businesses that are similar to yours but aren’t competitors — like companies in a different market or geographical location — and asking what figures they use. The business projects that its sales will increase by 20% next year, resulting in projected sales of $1,200,000. One of your goals as a business owner is to increase your sales percentage to grow your business and stay competitive.

Get the figures together

While COGS is generally related to sales, it might not directly correspond to changes in sales volume. This could happen because of factors like inventory accounting methods or changes in material costs. But you need to link these to implement the percentage of sales method. In this article, we’ll explain the percentage of sales method and how to calculate it. We’ll also show you a real-life example, highlighting its benefits and drawbacks.

The percentage-of-sales method is a financial forecasting model that assesses a company’s financial future by making financial forecasts based on monthly sales revenue and current sales data.

Liz looks through her records for the month and calculates her total sales at $60,000.

When the percentage-of-sales method doesn’t cut it, there are a couple more ways to determine a business’ financial outlook.

She decides she wants to put together a rough financial forecast for the future, so she opts to leverage the percent of sales method.

How to estimate your allowance

Frank wants to see the percentage of sales for his expenses specifically so he goes back to his initial amounts and sees that expenses totaled $20,000, or 20% of revenue. Divide your line item amounts by the total sales revenue amount to get your percentage. When the percentage-of-sales method doesn’t cut it, there are a couple more ways to determine a business’ financial outlook.

Larger companies allow for a certain percentage of bad credit in their financial analysis, but many small businesses don’t, and it can lead to unrealistic projections and unforeseen loss. The percentage of sales method allows businesses to make accurate assessments of their previous sales so they can comfortably project into the future. The percentage of sales method allows you to forecast financial changes based on previous sales and spending accounts. Multiplying the forecasted accounts receivable with the historical collection patterns will predict how much is expected to be collected in that time period.

And second, it can yield high-quality forecasts for those items that closely correlate with sales. This takes the credit sales method a step further by calculating roughly how much a company can expect not to be paid back from customers if they haven’t paid their credit sales after 90 days. Tracking the ratio is helpful for financial analysis as the store might need to change its credit sales policy or collections process if the ratio gets too high.

Important Formulas Used in PoC Calculations

It also can’t consider other financial changes like future bad debts that might impact sales. Because the percentage-of-sales method uses common financial ratios and percentages, it’s a good tool for quickly comparing how a company is doing compared to its competitors or the wider market. Finally, it’s important to note that the PoC method leaves the door open for malfeasance by unethical actors. Of course, every accounting method has its vulnerabilities, and employees or companies can often find a way to exploit any system. However, PoC can be especially vulnerable to so-called “creative accounting” because it is inherently based on estimations spread across multiple time periods.

Easy to compare across businesses

Adopting smart strategies can improve your sales performance and boost your revenue. While it offers a good starting point, it’s essential to use this method alongside other forecasting techniques. With changing budgets and different needs every month, it’s important to know where your money is going and how it affects future earnings. Read our ultimate guide on white space analysis, its benefits, and how it can uncover new opportunities for your business today. She estimates that approximately 2 percent of her credit sales may come back faulty.

There’s no standard percentage used to estimate bad debts in any of the formulas.

Outside of these items, it is better to develop a detailed, line-by-line forecast that incorporates other factors than just the sales level.

Checking up to see how the actual figure is progressing against the predicted one helps to manage accounts receivable accordingly and tighten collection processes for businesses.

But you need to link these to implement the percentage of sales method.

It can be applicable to a wide variety of situations, including for software companies that create custom products for clients that require ongoing development and frequent modifications.

It’s a contra-receivable account that reduces the value of your receivables and overall assets.

This information about past sales data helps you predict future financial performance.

On disposal, reclassification ensures that the amount recognised in SOPL will be consistent with the amounts that would be recognised in SOPL if the financial asset had been measured at amortised cost. Available for sale securities are securities that are available for sale (literally!) and have a readily available market price. At the end of each financial year, companies need to value the available for sale securities. Any gains/losses due to the change in valuation are not included in the Income Statement but are reflected in the Statement of Comprehensive Income.

Transform how you see, plan and lead your business

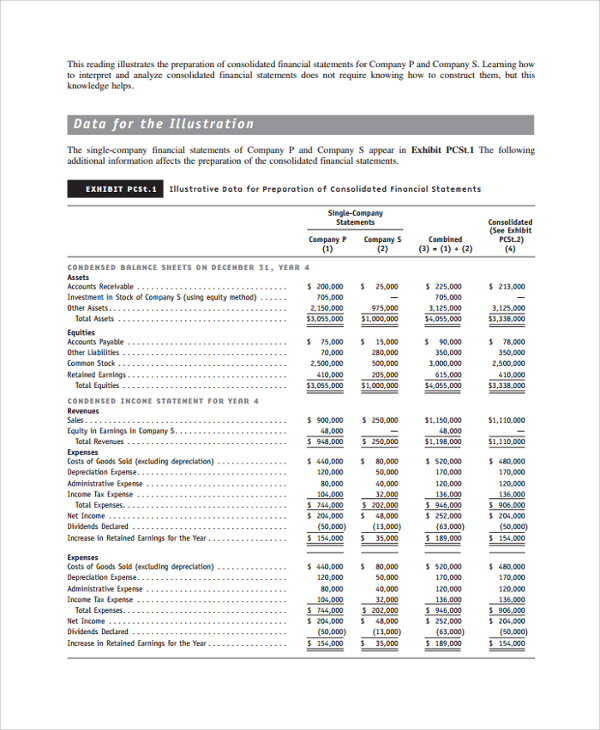

Answer Let’s consider each of the investments in turn to determine if control exists and, therefore, if they should be accounted for as a subsidiary. A typical OT question may describe a number of different investments and you would need to decide if they are subsidiaries – i.e. if control exists. The following income statements have been produced by P and S for the year ended 31 March 20X9. Once any impairment has been identified during the year, thecharge for the year will be passed through the consolidated incomestatement.

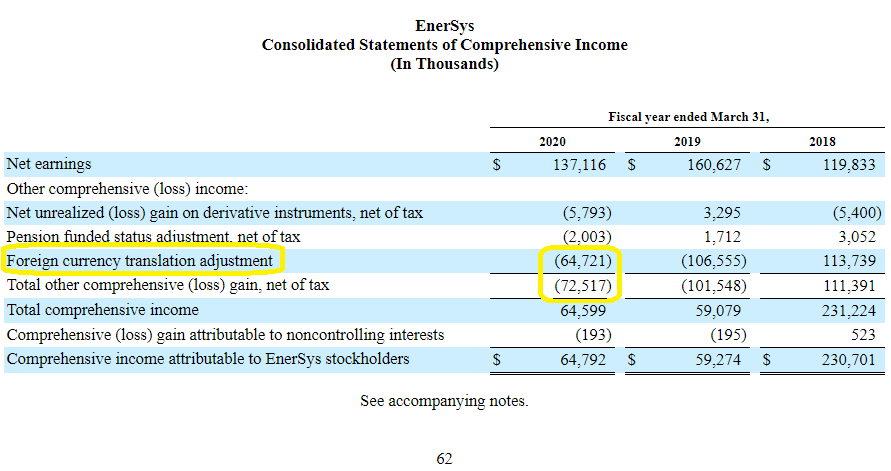

Statement of Comprehensive Income

This approach provides a more comprehensive view of the parent company’s financial performance, reflecting its interest in the profits generated by its subsidiaries, regardless of whether those profits are distributed as dividends. Separate financial statements report the financial performance of individual entities, while consolidated financial statements merge the financial data of a parent company and its subsidiaries into a unified report. Consolidated statements eliminate internal transactions, providing a comprehensive view of the entire group.

Companies with consolidated financial statements

For fully consolidated statements—where all a subsidiary’s assets and liabilities are rolled into the parent’s statement—there won’t be separate line items showing subsidiaries.

Set out below are the draft income statements of P and its subsidiary S for the year ended 31 December 20X7.

For example, gains on the revaluation of land and buildings accounted for in accordance with IAS 16, Property Plant and Equipment (IAS 16 PPE), are recognised in OCI and accumulate in equity in Other Components of Equity (OCE).

A consolidated financial statement is a group of financial statements of a parent company and its divisions and/or subsidiaries.

This could be asked as an OT question but is more likely to be a MTQ where you will be calculating and submitting a figure for each of the component parts of the goodwill calculation – cost, NCI and net assets.

To understand this, we must first pay heed to the opposite of comprehensive income.

Both GAAP and IFRS have some specific guidelines for entities that choose to report consolidated financial statements with subsidiaries. Unrealized gains or losses can make consolidated financial statements inaccurate, especially if they result from intercompany transactions. These adjustments ensure that the financial statements reflect only realized gains and losses from external transactions.

Specifically, it is located under the equity section of the balance sheet as well as under a related statement called the consolidated statement of equity. A revaluation surplus on a financial asset classified as FVTOCI is a good example of a bridging gain. The asset is accounted for at fair value on the statement of financial position but effectively at cost in SOPL. As such, by recognising the revaluation surplus in OCI, the OCI is acting as a bridge between the statement of financial position and the SOPL.

This ensures that a company’s financial data is always clean, accurate, and readily available for reporting. Existing disclosures to either detail comprehensive income and all of its components at the bottom of the income statement, or on the following page in a separate schedule, have made analysis easier. A number of accountants have questioned why OCI is listed as part of equity on the balance sheet, but if you look carefully, there are a number of places to locate it and help determine the health and total economics of the underlying company. Insurance companies like MetLife, banks, and other financial institutions have large investment portfolios. In this respect, OCI can help an analyst get to a more accurate measure of the fair value of a company’s investments. This statement illustrates the changes in equity of the parent company and its subsidiaries over a specific period.

At the end of the statement is the comprehensive income total, which is the sum of net income and other comprehensive income. Comprehensive income is the sum of a company’s net income and other comprehensive income. Concluding exam tips Remember that at FA/FFA level, a good solid platform of understanding the principles consolidated statements of comprehensive income of consolidation is required. IAS 28 also states that a holding of 20% or more of the ordinary (voting) shares can be presumed to give the investor significant influence unless it can be demonstrated otherwise. You should use the range 20-50% of voting shares in the exam as your main indicator of significant influence.

In this question the fair value of the non-controlling interest is given, so in our calculation we just need to add it to the consideration transferred. In a MTQ it is likely you would be given the value of a NCI share and have to apply it to the 8,000 shares that Red Co did not acquire. However, in this particular question, by reading the question carefully you will see that eliminating the unrealised profit was a red herring as we were simply being asked for the consolidated revenue.

Please let us know if you are planning a move, otherwise we will assume your tax status has changed and may have to deduct UK income tax from your payment. In some instances, the level of UK income tax that OUP is required to withhold from your payment may change, depending on your new country of residence. If your new country requires that you report your royalty income, we will have to deposit your payment into a bank account in that country.

Any performance of music by singers or bands requires that it be first reduced to its written sheet form from which the « song » (score) and its lyric are read.

Sometimes, a royalty percentage is computed and then paid to the owner.

Otherwise, the authenticity of its origin, essential for copyright claims, will be lost, as was the case with folk songs and American « westerns » propagated by the oral tradition.

While the player piano made inroads deep into the 20th century, more music was reproduced through radio and the phonograph, leading to new forms of royalty payments, and leading to the decline of sheet music.

The term « royalty » refers to the amount due to use the benefits of certain rights granted to other individuals.

For example, if calculated royalty is Rs. 900,000/- as per sale of books based on the above example, but royalty payable is Rs. 1000,000 as per minimum rent, shortworking will be Rs. 100,000 (Rs. 1,000,000 – Rs. 9,00,000).

The Income approach focuses on the licensor estimating the profits generated by the licensee and obtaining an appropriate share of the generated profit. It is unrelated to costs of technology development or the costs of competing technologies. A similar http://dninasledia.ru/v-seti-poyavilis-foto-roskoshnoj-kvartiry-ivanki-tramp/ approach is used when custom software is licensed (an in-license, i.e. an incoming license). The product is accepted on a royalty schedule depending on the software meeting set stage-wise specifications with acceptable error levels in performance tests.

Royalty Meaning in Accounting

The royalty due to the developer is 4,000 (500 x 8.00), and the publisher posts the following journal entry to record the payment. Short Workings is nothing but the amount by which the minimum rent is more than the actual royalty. In other words, short workings is the difference between minimum rent and actual royalty. In other words, when there is no or little production or sale, the lessor would be at a loss since no or less amount of royalty would be received from the lessee. Although, the user of asset pays consideration to the owner for using the owner’s asset both in the case of acquiring a property on rent or a book for publishing. For example, if royalty amount is 1,000,000/-& rate of TDS is 10%, then lessee will pay Rs. 900,000/- to lessor.

The licensor’s share of the income is usually set by the « 25% rule of thumb », which is said to be even used by tax authorities in the US and Europe for arms-length transactions. Even where such division is held contentious, the rule can still be the starting point of negotiations. The latter is more than mere access to secret technical or a trade right to accomplish an objective. It is, in the last decade of the past century, and the first of this one of the major means of technology transfer.

Most Inspiring Products for Old People are Great New Products for You, Too.

Another reason that a royalty recipient may see a “Balance Forward” on their statement is due to advances. Until this advance is earned out, the unearned balance will appear as a negative balance forward when accouting for royalty payments. In 2017, a government consultation regarding the impact of the digital economy resulted in tweaks to royalty taxation. Under the current system, companies making royalty payments in specific areas will need to deduct withholding tax at 20% from those royalties.

Most schemes prescribe a minimum amount that the artwork must receive before the artist can invoke resale rights (usually the hammer price or price). Some countries prescribe and others such as Australia, do not prescribe, the maximum royalty that can be received. Some country’s prescribe a sole monopoly collection service agency, while others like the UK and France, allow multiple agencies.

Statement detail

Thus a music download was a « copy » of proprietary music and hence required to be licensed. An inter-active service is one which allows a listener to receive a specially created internet stream in which she dictates the songs to be played by selecting songs from the website menu. Such a service would take the website http://linko.co.ua/svyato-nablizhayetsya-zrobit-sobi-podarunok out from under the compulsory license and require negotiations with the copyright owners. Typically, the PRO negotiates blanket licenses with radio stations, television networks and other « music users », each of whom receives the right to perform any of the music in the repertoire of the PRO for a set sum of money.

The portion of the realizable profit that should be credited to the invention as distinguished from non-patented elements, the manufacturing process, business risks, or significant features or improvements added by the infringer. The portion of the profit or of the selling price that may be customary in the particular business or in comparable businesses to allow for the use of the invention or analogous inventions. The nature of the patented invention, the character of the http://all-photo.ru/empire/index.en.html?img=8629&big=on commercial embodiment of it as owned and produced by the licensor; and the benefits to those who have used the invention. In period 1, 500 copies of the game are sold and the developer earns 4,000 in royalties and makes the following posting. Using the same information from the example above, the developer would make the following bookkeeping entries to record the transactions. Therefore, in the following years Short Workings is adjusted against the excess royalty amount.